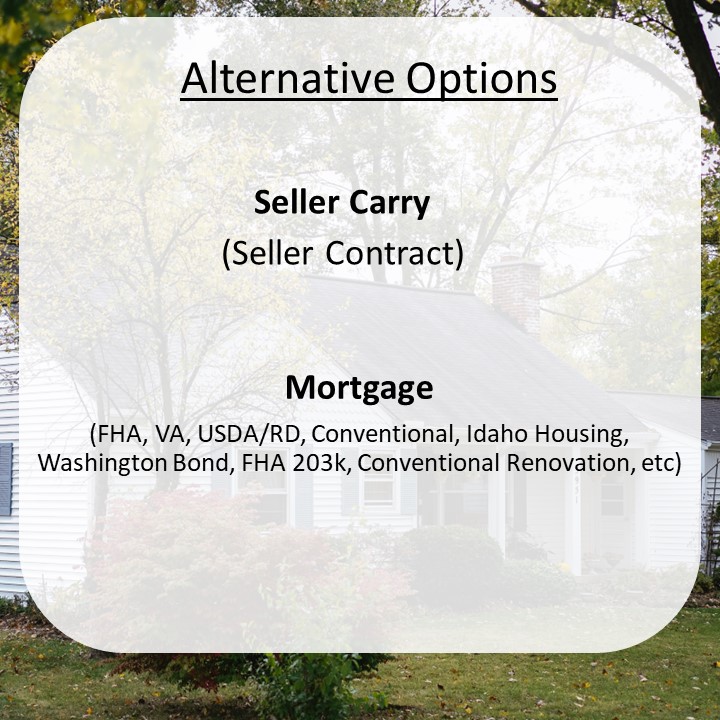

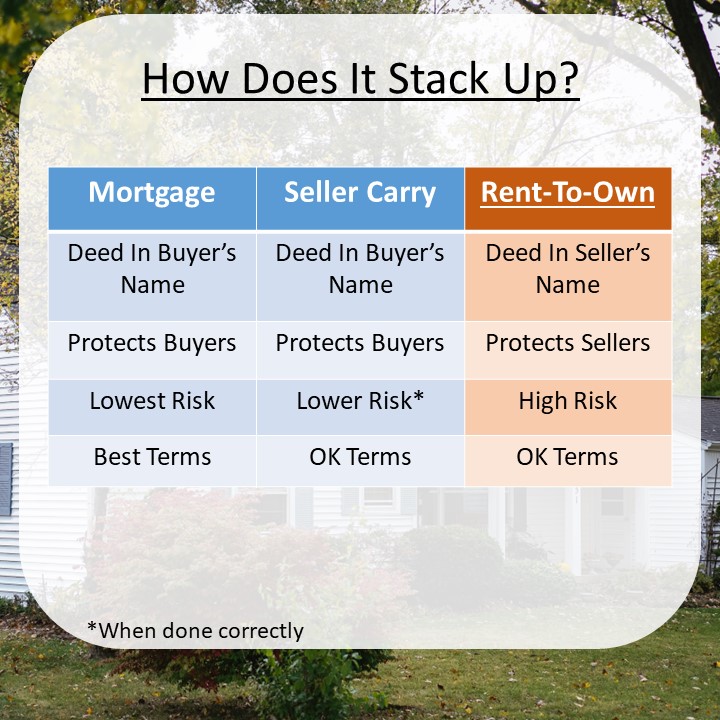

Seller Carry Contracts

A Look At Seller Carried Contracts A seller carried contract is something I see more often with vacant land, but it can be used for…

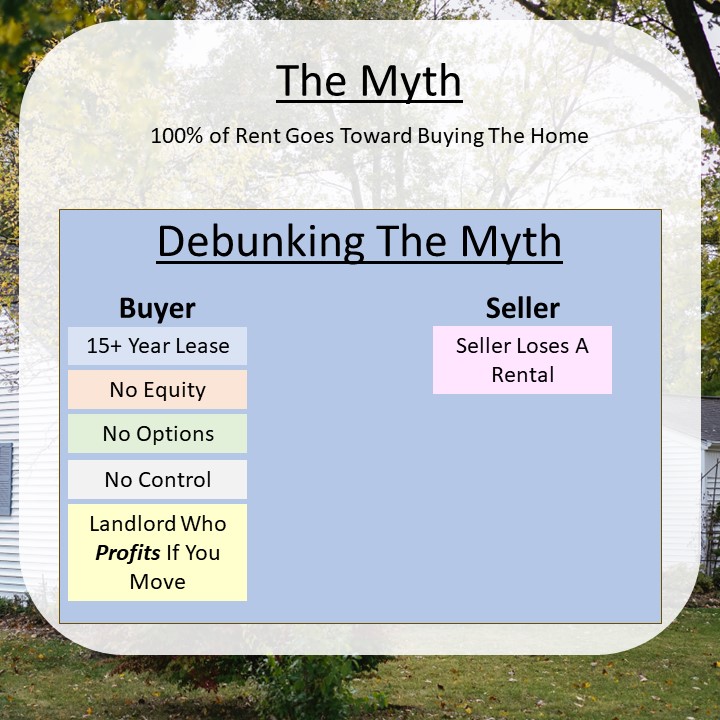

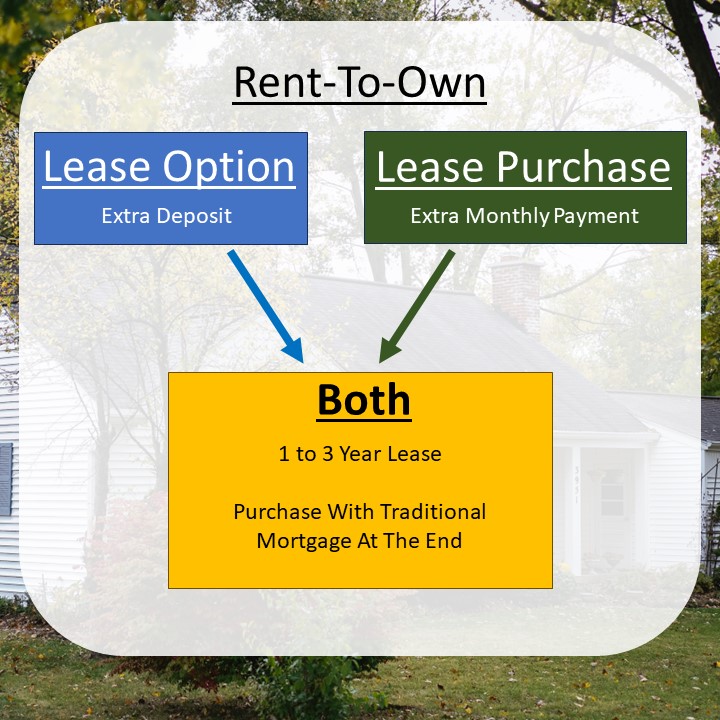

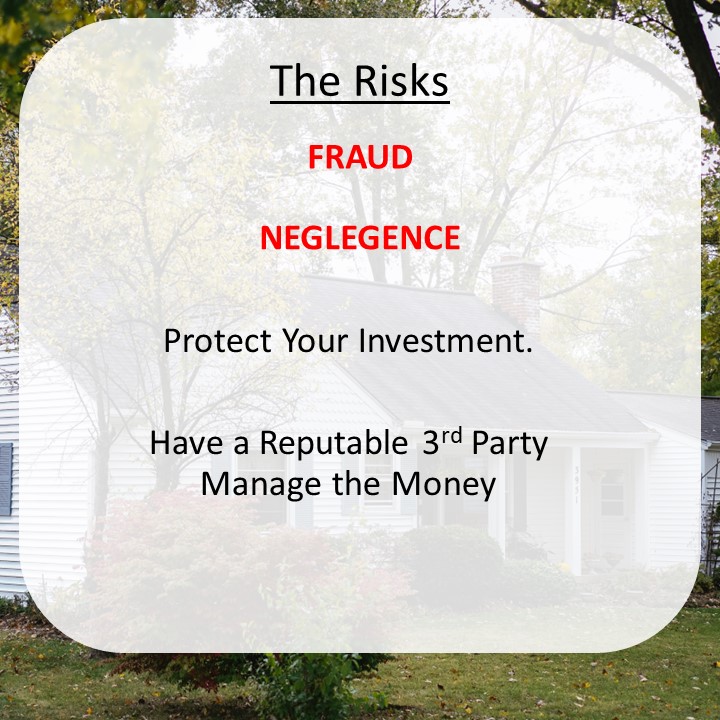

Rent-To-Own

A Look At The Inland Northwest…. Every year, I get several inquires about properties that would possibly sell as a rent-to-own. For many of these…

Idaho OR Washington: Which Is A Better Fit For You?

A Look At The Inland Northwest…. North Idaho and Eastern Washington are close neighbors with some pretty fundamental differences. From Gun Laws to Marijuana Laws,…